Ever looked at your credit card processing statement and felt like you needed a financial Rosetta Stone to decode it? You're far from alone. Credit card processing fees are intentionally complex, but grasping the core pricing models is the first step toward controlling your business costs.

One of the most transparent and widely trusted structures—especially among larger merchants—is Interchange Plus Plus (Interchange++). Here’s what those two “pluses” actually mean and how they affect your bottom line.

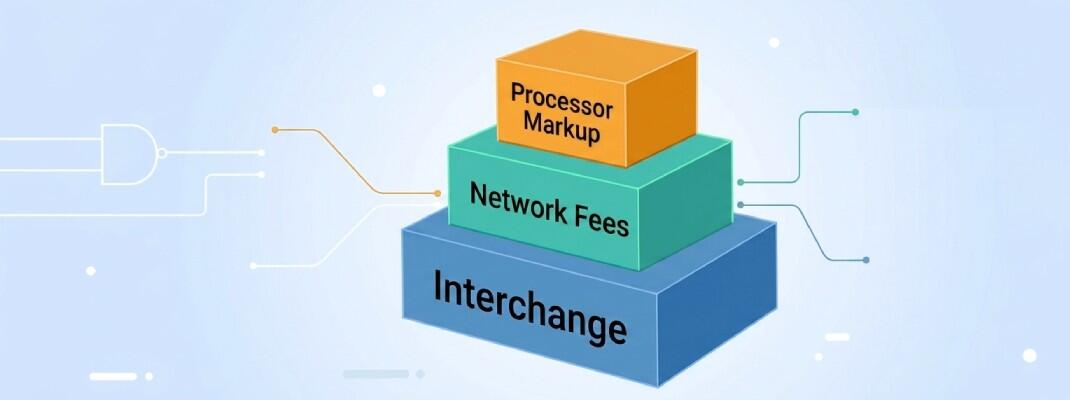

What Is Interchange Plus Plus (Interchange++)?

Interchange++ separates the three fundamental cost components of every credit card transaction. Instead of bundling fees together the way tiered pricing does, this model itemizes each part so you can see exactly where your money is going.

1. Interchange: The Foundation Cost

Interchange is the base cost of running a card transaction.

- Charged by: The card-issuing bank (your customer’s bank)

- Received by: The issuing bank

Interchange rates are set directly by Visa and Mastercard, making them completely non-negotiable. They vary based on:

- Card Type: Rewards, corporate, and premium cards cost more than basic debit cards.

- Transaction Method: Swiped/EMV, tap-to-pay, online, or keyed-in all have different rates.

- Merchant Category Code (MCC): Your industry classification affects pricing.

- Data Security: More data (AVS, CVV, Level 2/3) can reduce interchange costs.

Important: Interchange is identical regardless of the processor you use.

2. The First Plus (+): Card Network & Assessment Fees

These are fees charged by the card networks for using their payment rails.

- Charged by: Visa, Mastercard, Discover, American Express

- Received by: The card networks

These small percentage-based fees (e.g., Visa Assessment Fee, Mastercard Network Access Fee) support transaction routing, authorization, and settlement functionality. Like interchange, they’re standardized and non-negotiable.

3. The Second Plus (++): The Processor’s Markup

This is the only part of your pricing that’s actually negotiable.

- Charged by: Your payment processor

- Received by: The payment processor

Markup usually appears as a small percentage plus a per-transaction fee (e.g., Interchange + 0.15% + $0.10). It covers technology, risk management, customer support, and profit.

Why Interchange++ Is the Most Transparent Pricing Model

- Full Transparency: You can clearly see interchange, network fees, and the processor’s markup.

- Negotiation Power: Since markup is visible, you can negotiate it directly.

- Cost Control: You can analyze which card types or transaction methods increase costs.

The Hidden Layer: “Custom Fixed Fees”

While the Interchange++ structure itself is transparent, processors—especially in high-risk industries—may add extra fixed fees. These flat charges can include:

- Monthly statement fees

- PCI compliance fees

- Gateway fees

- Batch fees

- Risk or monitoring fees

Always request a complete breakdown of all fees, beyond just the Interchange++ markup. Real transparency means understanding every line item on your statement.

Final Thoughts

Understanding the Interchange++ model puts you in control of your payment processing expenses. With a clear view of what’s negotiable—and what isn’t—you can secure better pricing, avoid unnecessary fees, and make informed decisions that protect your profitability.